Disclaimer: The Blog on ‘Reproduction Cost’ is not a recommendation to buy / hold / sell any stock. The published post is for information purpose only. Please read the detailed disclaimer at the bottom of the post.

How to Calculate the Replacement Cost of a Company

This article is an excerpt from the well-known book ‘From Graham to Buffett and Beyond’. The 4th Chapter of the book explains in detail how can we calculate the Reproduction cost (i.e. Replacement cost) of a company, i.e. the cost for setting up a new similar company. The following is a summary of the same.

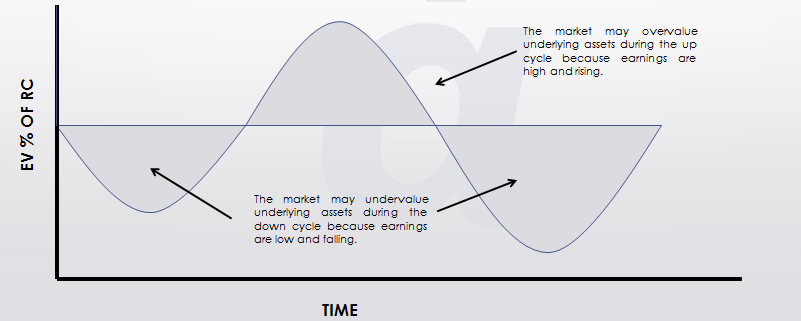

Based on Industry Trends:

- If the industry is in downturn, assets should be valued at what they will bring in at liquidation. As it will be hard to find a buyer in the industry downturn and hence they would be sold at scrap prices.

- However, if the industry is stable or moving upwards, the assets in use will be needed to be reproduced as they wear out, and hence they should be valued at their reproduction cost.

Reproduction Costs Calculation for Various Line Items:

Current Assets:

The adjustments to current assets won’t be much, and won’t matter much in most cases.

Accounts Receivable:

There would be some bad debts mentioned in the notes. A new company is more likely to get higher bad debts, so the cost of reproducing accounts receivables is probably higher than the company’s Balance Sheet number.

Inventory:

For manufacturing company, more commodity-like the inventory, lesser discount should be given to it. Eg: Cotton yarn can be sold at fair value easily rather than a tie-dyed T-shirt.

-

- If inventory is been piling up, i.e. if it equals 150 days’ worth of cost of goods sold in current year, compared to last year’s 100 days, then the additional 50 days may represent items that will never sell or will sell only at closeout prices.

- Also, if the company uses LIFO (Last-In-First-Out) to account the inventory, then the actual worth of inventory would be higher than the Balance Sheet number by the amount called ‘LIFO Reserve’ (the amount by which the current cost of any item exceeds the old).

Property, Plant and Equipment:

-

- Property: Assets like buildings will be worth far more, relative to their book value.

- Plant & Equipment: The difference between the reproduction cost of the plant and the number mentioned in the Balance Sheet is huge, due to 2 reasons:

- Depreciation rules the company follows might bear hardly any resemblance to what actually is the economic value of the asset. Eg: Telecom infrastructure might last for decades but the company would have depreciated it to zero over short span of time comparatively.

- Inflation: Depreciation is based on historical cost of the plant, which would be too high currently owing to inflation. So our depreciation numbers in the Income Statement might be quite smaller compared to a company who would set up a new plant recently. However, in a high-tech innovative industry, new entrant might have more state-of-the-art tools.

Intangible Asset:

Surest method for assigning value to license/franchise is to look for values of similar license/franchises. Also, it can be calculated on ‘per unit’ basis.

Goodwill:

Any potential competitor will have to pay dearly for the value of the brand, consumer loyalty, distribution networks, etc.

Subsidiary Valuation:

Similar to per unit approach. But instead of price per unit, the multiple would be cash flow per unit or EBIDTA per unit.

Others:

-

- R&D Cost: Eg: Boeing spent ~4% of its revenues as R&D cost, and its assets last for 15 years. This signifies a new competitor will have to spend 55-60% (~4×15) of its current annual sales to match Boeing’s range of production.

- Developing customer relationship also costs money, which never appears as an asset. A new company needs to spend on the sales cycle. How many months of SG&A expenses the company has to pay out before it starts to take orders and generate revenue, needs to be added. Also, the company needs to build the internal system that helps it to allow to function, specially systems which include IT, human resource policies, and other unglamorous but essential procedures. So we need to add multiple of SG&A line, in most cases between 1-3 years’ worth, to the reproduction cost of the assets.

Liabilities:

-

- We can simply subtract the book value of current liabilities from the reproduction value of total assets to arrive at the reproduction value of net assets.

- Liabilities that arise from past circumstances: Eg – Deferred Tax Liabilities, etc. will have to be subtracted from the asset value.

- Debt: We use market value of debt to subtract it from the assets.

In the above case, post subtracting the assets by the 1st two categories of liabilities, we reach net asset value to which investors (debt & equity) have claims.

Graham and Dodd Net-Net Approach (Bullet-Proof Approach):

All Liabilities are subtracted from Current Assets to arrive at a conservative figure that is hard to beat and more difficult to find a company available at or below that valuation.

Simple Companies produce financial statements with no place to hide. Whereas complicated company’s financial statements are full of dark corners which might be potentially rich in treasure and unidentified value.

Disclaimers :

The information herein is used as per the available sources of bseindia.com, company’s annual reports & other public database sources. Alpha Invesco is not responsible for any discrepancy in the above mentioned data. Investors should seek advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents

Future estimates mentioned herein are personal opinions & views of the author. For queries / grievances – support@alphainvesco.com or call our support desk at 020-65108952.

SEBI registration No : INA000003106

Readers are responsible for all outcomes arising of buying / selling of particular scrip / scrips mentioned here in. This report indicates opinion of the author & is not a recommendation to buy or sell securities. Alpha Invesco & its representatives do not have any vested interest in above mentioned securities at the time of this publication, and none of its directors, associates have any positions / financial interest in the securities mentioned above.

Alpha Invesco, or it’s associates are not paid or compensated at any point of time, or in last 12 months by any way from the companies mentioned in the report.

Alpha Invesco & it’s representatives do not have more than 1% of the company’s total shareholding. Company ownership of the stock : No, Served as a director / employee of the mentioned companies in the report : No. Any material conflict of interest at the time of publishing the report : No.

The views expressed in this post accurately reflect the authors personal views about any and all of the subject securities or issuers; and no part of the compensations, if any was, is or will be, directly or indirectly, related to the specific recommendation or views expressed in the report.

Stay Updated With Our Market Insights.

Our Weekly Newsletter Keeps You Updated On Sectors & Stocks That Our Research Desk Is Currently Reading & Common Sense Approach That Works In Real Investment World.